By 2030, the most valuable U.S. energy retailers, especially in Texas, will look far less like commodity suppliers and far more like data-driven service platforms. In place of a narrow focus on cents per kWh, leaders will compete on intelligence, trust, and outcomes. They will orchestrate distributed energy resources at scale, operate portfolios as virtual power plants, and deliver what commercial and industrial buyers actually purchase, which is, uptime, emissions progress, and cost certainty.

Think of the future retailer in three parts:

- First, flexibility is the product where multi-gigawatt virtual power plants are built from thousands of C&I sites, dispatched as a single portfolio with verifiable performance.

- Second, data is the orchestration fabric. Interoperable systems that move trusted telemetry from device to settlement, with models that learn hour by hour and improve the hedge, not just the report.

- Third, resilience is the promise where customers will pay for fewer outages, quicker recoveries, and higher power quality, especially as Texas adds data centers, EV manufacturing, and other power-dense industries.

Cybersecurity sits underneath all three. In a grid full of smart endpoints, a device breach is a market risk; leaders are building defense-in-depth from sensor identity to market interface and treating data integrity with the same seriousness as financial controls.

The New Customer Relationship

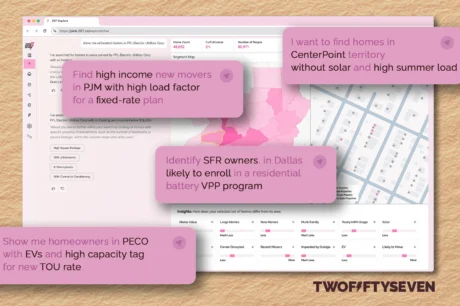

In ERCOT’s unforgiving mix of thin margins and frequent volatility, survival has always depended on speed and precision. What’s changing is the operating model behind that speed. Retailers are knitting together telemetry from meters and devices with market signals, weather, and site operations. They’re using real-time data to forecast exposure at the node, shape load before price spikes hit, and automate bids into day-ahead and ancillary markets. Flexibility stops being a once-in-a-while demand response event and becomes a core product that is planned, dispatched, measured, and settled like any other capacity.

This shift is driven as much by customers as by markets. Large C&I buyers are layering in onsite solar and storage, adding controls to major loads, and asking for Energy-as-a-Service structures that balance price stability with renewable guarantees. They don’t just want a better bill; they want fewer bad days. The retailer’s new role is to orchestrate everything behind the meter, like HVAC, refrigeration, process loads, batteries, and backup generation, so that energy decisions align with production schedules and SLAs. That orchestration only works when the data is clean; the baselines are credible, and the automation respects the physics and safety of each facility.

The Changing P&L

This evolution changes the P&L. By the latter half of the decade, a growing share of margin will come from software and services: optimization, analytics, forecasting, and asset management layered on top of commodity supply. The spread still matters, hedging discipline and portfolio construction never go out of style, but the durable value comes from intelligence and integration.

What does it take to get from here to there? In practical terms, retailers need to build for data-enabled flexibility now. That means:

Deploy compliant aggregation infrastructure — Digitize telemetry, metering, and settlements across C&I portfolios, ensuring every controllable resource is both addressable and auditable.

Turn customers into capacity — Unlock HVAC, refrigeration, compressed air, process loads, backup generation, and storage with automation that respects constraints and proves baselines.

Monetize the data exhaust — Use AI to detect anomalies, optimize power factor, and forecast price exposure at the node, not just the zone.

Partner strategically — Form joint programs with customers and technology providers: co-invest in batteries and controls, integrate building-management systems with market operations, and extend carbon-intensity reporting down to the shift level.

The Build Year Is Now

For Texas C&I retailers, 2025 is the build year. The foundations for them being flexible market participation, interoperable data plumbing, cyber-resilient operations, and customer-centric service design. These cannot be bolted on later. In a market that punishes hesitation and rewards speed, the time is to invest now so that retailers are not merely weathering ERCOT’s volatility but leading it.

Compete on Intelligence: Partner with ESG

If you’re serious about competing on flexibility and data, make ESG your operating system for C&I portfolios. ESG is built for exactly this moment in ERCOT: data-enabled flexibility, market-grade settlement, and customer-centered resilience, packaged as software you can deploy, not slides you can admire.